Canada Pension Plan Investment Board (CPPIB) plans to invest about 1 billion reais ($396 million) in commercial property in Brazil, a few months after the Toronto-based pension fund opened an office in São Paulo.

In a statement released late on Monday, CPPIB said the investments include the purchase of warehouses, land and stakes in development projects in the logistics and retailing industries, adding to the fund's portfolio of more than 100 properties in Latin America's largest economy.

The move brings CPPIB's real estate commitments in Brazil to over $1.8 billion. Since 2009, CPPIB has bought real estate in Brazil to profit from rising demand for corporate and distribution facilities. The Canadian giant, one of the world's biggest pension funds with more than $212 billion in assets under management, opened an office in Brazil in February to gain on-the-ground presence and business connections before tapping complex, sizeable investment opportunities. CPPIB's São Paulo office focuses primarily on investments in Brazil, Chile, Colombia, Mexico and Peru.

"Brazil remains a key market for CPPIB over the long term and we will continue to seek attractive investment opportunities through our existing partnerships with top-tier local partners while we continue to build our local presence in Sao Paulo," Peter Ballon, head of CPPIB's real estate investment in the Americas, said in the statement.

CPPIB will pay 507 million reais for 30 percent in a joint venture with Singapore's Global Logistic Properties Ltd. , the world's No. 2 owner of industrial properties, to run 32 logistics properties in São Paulo and Rio de Janeiro, the statement added.

Another 231 million reais were committed to GLP Brazil Development Partners I, a real estate investment vehicle in which Global Logistic Properties has a 40 percent stake and CPPIB a 39.6 percent stake.

CPPIB also pledged to spend 159 million reais to buy a 25 percent stake in a São Paulo logistics project alongside Cyrela Commercial Properties SA.

The fund also paid 100 million reais for a 33.3 percent stake in the Santana Parque Shopping mall, which is jointly run by partner Aliansce Shopping Centers SA, the statement added. CPPIB has a 27.6 percent in Aliansce, a shopping mall operator.

In a separate statement, the pension fund announced that Rodolfo Spielmann was named general director and leader of CPPIB's operations in Latin America. Spielmann, a former Deutsche Bank AG banker and a Bain & Co executive in Brazil for the past 14 years, started at the fund on Oct. 20.

CPPIB has committed $5.6 billion to investments in Latin America.

The Canada Pension Plan Investment Board (CPPIB) has announced a combined $445 million of investments in logistics and retail assets in Brazil in a string of moves that bring its real estate commitments in the South American giant to more than $2 billion.

“Since making our first real estate investment in Brazil in 2009, CPPIB has become one of the largest investors in the sector with ownership interests in logistics, retail, office and residential assets or developments,” Peter Ballon, managing director and head of real estate investments — Americas, said in a release Monday.

“Over the past 10 months we deepened relationships with our key partners to commit additional equity in high-quality real estate assets that are important additions to our diversified Brazilian portfolio.”

The latest investments include $226 million in a joint venture with Global Logistic Properties to invest in a portfolio of 32 logistics properties that GLP previously acquired from BR Properties S.A. CPPIB will have a 30 per cent ownership stake in the joint venture. Logistics properties include warehouses, distribution facilities and the like.

Meanwhile, the CPPIB has committed an additional $103 million to GLP Brazil Development Partners I, an existing joint venture that is owned 40 per cent by GLP, 39.6 per cent by CPPIB and 20.4 per cent by the Government of Singapore Investment Corp. The additional capital will be used to acquire a strategically positioned land parcel in Rio de Janeiro comprising 3.8 million square feet of buildable area.

It has also committed $71 million to acquire a 25 per cent interest in a new logistics development project alongside longtime partner Cyrela Commercial Properties. Called Cajamar III, the development will comprise more than 2.7 million square feet of leasable area located on the outskirts of Sao Paulo.

And the CPPIB is acquiring a 33.3 per cent interest in Santana Parque Shopping for $45 million. Aliansce Shopping Centers, an existing partner, also owns a 33.3 per cent interest in the 280,000 square foot regional shopping centre in Sao Paulo.

“Brazil remains a key market for CPPIB over the long term and we will continue to seek attractive investment opportunities through our existing partnerships with top-tier local partners while we continue to build our local presence in Sao Paulo,” Ballon said.

Canada Pension Plan Investment Board is a professional investment management organization that invests the funds not needed by the Canada Pension Plan to pay current benefits on behalf of 18 million Canadian contributors and beneficiaries.

Soon after the news of this Brazilian transaction broke out, the critics came out swinging. Canada's Business News Network invited Jim Doak, President and Managing Partner of Megantic Asset Management, who said he was "suspicious" and "had a bad feeling about this." He questioned the valuations of illiquid investments and said he's "smelling ego here" and the CPPIB is taking on serious foreign country risk (watch the entire BNN clip here).

I don't know where BNN finds these people to comment on pension fund deals but this guy sounds like Andrew Coyne when he railed against the CPPIB in his comment on Ontario's new pension suckers. In fact, take a look at this snapshot I took on my computer from the BNN interview (click on image):

You'll see other clips with a negative spin on the CPPIB and their "expensive" and "complex" operations. Of course, they don't mention how CPPIB's governance is one of the best in the world and how they have been very careful investing in private markets in this environment, fully cognizant that deals are pricey.

Now, let me share my thoughts on this Brazilian real estate deal. From a timing perspective, this deal couldn't come at a worse time. Why? Because the Brazilian economy remains in recession and things can get a lot worse for Latin American countries which experienced a boom/ bust from the Fed's policies and China's over-investment cycle. This is why some are calling it Latin America's 'made in the USA' 2014 recession, and if you think it's over, think again. John Maudin's latest, A Scary Story for Emerging Markets, discusses how the end of QE and the surge in the mighty greenback can lead to a sea change in the global economy and another emerging markets crisis.

Mac Margolis, a Bloomberg View contributor in Rio de Janeiro, also wrote an excellent comment this week on why the oil bust has Brazil in deep water, going over the problems at Petroleo Brasileiro (PBR). A look at the one-year chart shows you a bit of how bad things are (click on image below):

You can say the same thing about Brazilian mining giant, Vale, which has also been pummeled in the last few months (click on image below):

The re-election of President Dilma Rousseff didn't exactly send a vote of confidence to markets as she now faces the challenge of delivering on campaign promises to expand social benefits for the poor while balancing a strained federal budget. President Rousseff says the Brazilian economy will recover and the country will avoid a credit downgrade but that remains to be seen. Having said all this, CPPIB is looking at Brazil as a very long-term play, so they don't care if things get worse in the short-run. In fact, the Fund will likely look to expand and buy more private assets in Brazil if things do get worse. And they aren't the only Canadian pension fund with large investments in Brazil. The Caisse also bought the Brazilian boom and so have others, including Ontario Teachers which bet big on Eike Batista and got out before getting burned. Are there risks to these private investments in Brazil? You bet. There is illiquidity risk, currency risk, political and regulatory risk but I trust CPPIB's managers weighed all these risks and still decided to go ahead with big investment because they think over the long-run, they will make significant gains in these investments. My biggest fear is how will emerging markets act as QE ends (for now) and I openly wonder if big investments in Brazil or other countries bound to oil and commodities are worth the risk now. Also, the correlation risk to Canadian markets is higher than we think. My only question to CPPIB's top brass is why not just wait a little longer and pick these Brazilian assets up even cheaper? But I already know what Mark Wiseman will tell me. CPPIB takes the long, long view and they are not looking at such deals for a quick buck. As far as "egos at CPPIB" that Mr. Doak mentions in the BNN interview, I can't speak for everyone there, but I can tell you Mark Wiseman doesn't have a huge ego. If you meet him, you'll come away thinking he's a very smart, humble and hard working guy who's very careful about the deals he enters.

Below, Reuters'Yiming Woo reports that Brazil's leftist President Dilma Rousseff narrowly re-elected in a vote that split along the country's social class and geography. I can't comment on President Rousseff except to say she will have big battles ahead, but I can tell you that Brazil is a great country with a bright future. Just like Neymar, it will rise and flourish again but the recovery could take a lot longer than CPPIB and others anticipate.

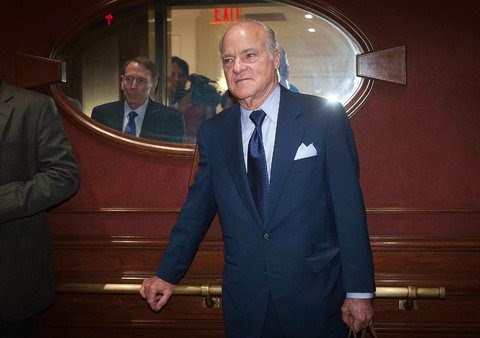

William A. Ackman, the silver-haired, silver-tongued hedge fund mogul, gestured out the window of a 42nd-floor conference room at Pershing Square Capital Management in Midtown Manhattan. The view was spectacular, but Mr. Ackman’s arm extended not downward, toward the vibrant fall foliage of Central Park, but skyward toward the top of a glittering glass building just around the corner on 57th Street.

He was pointing toward One57, a new 90-story, lavish hotel and condominium building described by one critic as “a luxury object for people who see the city as their private snow globe.” Specifically, Mr. Ackman was referring to the penthouse apartment. Named the Winter Garden, for a curved glass atrium that opens to the sky, it is a 13,500-square-foot duplex with an eagle’s-eye view of the park.

And it will belong to Mr. Ackman. When the sale closes, the reported $90 million price would be the highest ever paid for a Manhattan apartment. It is, he explained, “the Mona Lisa of apartments.” Never will there be another like it.

But Mr. Ackman, 48, doesn’t intend to live there. He lives at the Beresford, off Central Park, with his wife and daughters. The Winter Garden is just another investment opportunity for him and a few others. “I thought it would be fun,” he said, “so myself and a couple of very good friends bought into this idea that someday, someone will really want it and they’ll let me know.” Maybe he will hold some parties there in the meantime.

Whether it’s a top-of-the-world apartment, an attack on a company or even his annual vacations with friends (the next trip is Navy SEAL training), Bill Ackman does everything big.

And this may be his biggest year yet. Overseeing more than $17 billion, his hedge fund is up 32 percent in a year when many other hedge funds are just breaking even. He recently completed a public offering of stock in Europe of part of Pershing Square, and while the shares are trading below the offering price, he still raised $2.7 billion that he can use to make more big bets. He’s also a driving force behind one of the biggest — and certainly the most controversial — potential mergers of the year: Valeant’s $53 billion hostile takeover bid for Allergan, the maker of Botox.

His critics agree that he’s big. They say he stands out for his big mouth and oversize ego, an accomplishment in the hedge fund world. (Even back in high school, his tennis teammates presented him with a T-shirt that read: “A closed mouth gathers no foot.”) Others warn that his fund has a risk of blowing up. His portfolio is made up of bets on less than a dozen companies. (The Allergan stake alone made up 37 percent of his fund earlier this fall, according to filings.) That means when things go bad, they can go really bad. That’s what happened when his $2 billion bet on Target through a separate fund lost 90 percent of its value at one point.

He has wagered $1 billion that Herbalife, the nutritional supplement company, will fail. So far, that bet hasn’t panned out, and even one of his closest advisers has called his theatrics on the subject — including a teary, three-hour rant this summer in front of nearly 500 people — a mistake.

But on that crisp fall morning at Pershing Square, Mr. Ackman was uncharacteristically taciturn. Reserved, even. Or maybe he was just a bit annoyed.

When asked if he has had to make bigger, riskier bets as his fund has grown, he answered, a bit petulantly: “We certainly have to make bigger investments, that’s definitely true. But not riskier investments.” Asked about failures, like the Target bet, he sighed deeply. “Target was a bad investment,” he said, “but out of 30 investments, I don’t know of another investor with as high a batting average.”

He certainly has an enviable long-term record: His funds, excluding the Target and four other separate funds, have returned 21 percent net of fees over 10 years, annualized. He has achieved it by going on the offensive. Mr. Ackman’s role as an activist hedge fund investor is to persuade other shareholders that he knows how to run companies better than current management does. This involves research, argument and, perhaps most important, a sensitivity to how every pronouncement and gesture will be perceived.

“I was angry at Carl Icahn for many years, as you know,” Mr. Ackman said of the longtime activist investor, when asked if he holds grudges. He swiped at his eye and added, lest the movement be misinterpreted: “My eye is tearing. It’s not emotion. I have a clogged tear duct.”

His attention to detail and persuasive powers will be especially important come December, when Allergan shareholders hold a special meeting. Mr. Ackman will urge them to replace a majority of the company’s board and to pave the way for approving the takeover by Valeant.

It’s a high-stakes move. And Mr. Ackman is all in for a big win. He is intensely competitive about everything, from memorizing two-letter words for Scrabble games to, as it turns out, owning apartments.

“It’s one of a kind,” he said of his trophy penthouse. “By the way,” he added, nodding down the street where other luxury towers are expected to be built, “these other buildings are not going to be as good.”

Commanding the Room

All successful people have stories to tell about what allowed them to achieve fabulousness. There is usually a moral. In the story that Mr. Ackman likes to tell, the moral is this: Never doubt Bill Ackman.

During his freshman year at Harvard, Mr. Ackman happened to read the application essay of the guy in the room next door. It was about why he hated Smurfs. Mr. Ackman thought it was really good, and an idea formed. He would write a book on how to write a college essay, drawing on examples and interviews with Ivy League admissions officers. On the advice of a family friend, he broadened his book to include information on college admissions and sent it off to publishers. The rejection letters piled up. He dropped the idea.

Later, two guys from Yale wrote a similar book called “Essays That Worked,” which would be featured in a New York Times article.

“I suffered extreme psychological torture,” Mr. Ackman recalled. The advice that the family friend gave, he added, had been bad. “I said, the next time I have a really good idea, I’m not going to listen just because someone is older than me.” Mr. Ackman continued, “It’s not going to stop me from going forward.”

Fresh out of Harvard Business School in 1992, Mr. Ackman went to work for his father, Lawrence Ackman, at his commercial real estate brokerage firm, Ackman-Ziff. But the young man was impatient. After just one week, and shrugging off advice that he first work for a veteran hedge fund manager, Mr. Ackman convinced his Harvard buddy David P. Berkowitz to start a hedge fund.

Cobbling together $3 million, the two started Gotham Partners. In a tiny office, they pored over corporate filings, hunting for undervalued companies. In 1998, Gotham started a hostile proxy fight against a small Ohio real estate holding company, First Union Real Estate Equity and Mortgage Investments. It took months of tussling before Gotham prevailed.

At Gotham, Mr. Ackman developed the methods he would use again and again. He went after big targets and took his battles into the public arena. Those techniques proved especially useful when he had sold short a company’s stock, betting on a collapse on the stock price.

His first foray into activist short-selling was in the spring of 2002, when he released a 48-page, scrupulously researched paper criticizing the management and reserve levels of the Federal Agricultural Mortgage Corporation. By that fall, Farmer Mac’s stock had tumbled, producing a quick win for Gotham, which had sold the agency’s stock short.

Mr. Ackman’s next short target, in late 2002, was the bond insurer MBIA, which he argued had backed billions of dollars of risky financing. It was a bet that would take years, hours of presentations to credit agencies and regulators, and a Wall Street financial crisis in 2007 before eventually paying off when MBIA’s stock started to collapse. Mr. Ackman’s bet was a huge success, netting just over $1 billion. But Gotham’s days were numbered.

Over the course of several years, Mr. Ackman struggled to right the troubled First Union, including an attempt to merge it with a failing golf operator that Gotham also owned. Investors started to voice concern. When a judge’s decision about the merger in late 2002 went against Gotham, the partners decided to wind down. The once highflying fund was done.

More than a decade later, Mr. Ackman accepts partial responsibility for Gotham’s demise. The problem, he said, was not its investments, which he argues ultimately paid off, but rather the strategy of investing in real estate, which was hard to sell quickly when investors wanted their money back. “I made a couple of strategic mistakes that, had I had more perspective, I wouldn’t have made,” he said.

About a year after Gotham closed, Mr. Ackman reappeared with a new fund, Pershing Square, and a $50 million seed investment from the Leucadia National Corporation. There would be a new focus: activist investing. At Gotham, he learned that he needed research and a story. At Pershing, he perfected the skill of telling that story to an audience of shareholders, corporate directors and the news media.

“He’s trying to create a theatrical setting where it’s not about the words, it’s about the dynamic, the action,” said J. Tomilson Hill, chief executive of Blackstone Alternative Asset Management, an investor in Pershing Square.

He charged quickly out of the gate, persuading Wendy’s to divest itself of the Canadian chain Tim Hortons. Then he got McDonald’s to sell some of its restaurants and buy back shares. It became clear that when Pershing Square announced a stake in a company, something big was going to happen, and the stock moved.

“Bill commands a room. He’s a tall guy, a good-looking guy. He draws all eyes to him when he speaks,” said Damien Park, the founder of Hedge Fund Solutions, which consults on activist campaigns but has not worked with Mr. Ackman. “Also, his ideas aren’t usually incremental in nature — asking a company to distribute cash or clean up a balance sheet. They’re usually quantum changes in a company.”

That was true of his 2007 mark on Target. In just two weeks, he raised $2 billion for a special fund to invest in just one stock. He wanted Target to sell its credit card business and restructure its real estate holdings. Target sold off part of its credit card business, but management disagreed with his real estate plan. Over the course of two years, Mr. Ackman waged a $10 million campaign to replace board members with himself and four others.

When shareholders voted against him in the spring of 2009, the defeat stung more than his reputation. By then, losses amounted to as much as 90 percent, and many investors in the special Pershing Square fund, including the fellow activist investor Daniel S. Loeb through his Third Point hedge fund, had asked for their money back. Mr. Ackman suffered another black eye a few years later with J. C. Penney. He won a seat on its board in 2011 and handpicked Ron Johnson, the head of Apple’s retail stores, to turn around the troubled retailer. But the efforts were botched; the company went from being profitable to losing $1.4 billion in 2013. Mr. Ackman resigned from the board in the summer of 2013, selling his stake at an estimated loss of $473 million.

“Every time I see him,” said Mr. Hill at Blackstone, “I say: ‘Bill, do me a favor. Stay away from retail.’ ”

Still, Mr. Ackman notched two of his biggest hits — General Growth Properties and Canadian Pacific — over the same period, helping to offset the reputational and financial losses from Target and J. C. Penney. Pershing estimates that Mr. Ackman’s original $65 million investment in General Growth, which operated commercial properties and has been restructured into three businesses, is now worth $3.3 billion. In Canadian Pacific, Mr. Ackman has so far tripled the value of his original investment after replacing the board and forcing through a turnaround.

His defenders argue that anyone with a fund as large as Pershing is going to have the occasional blunder. “In this business, if you don’t make mistakes, you’re either a liar or you don’t take many swings at the ball,” said Leon Cooperman, the founder of the hedge fund Omega Advisors.

Always a Competition

Last year, Mr. Ackman and some friends took a scuba-diving trip off the coast of Myanmar. The sun was warm, the ocean calm, but even in this idyllic setting, Mr. Ackman felt compelled to devise a competition he could win. After surfacing from each dive, he checked his air gauge against everyone else’s, to see who had used the least amount of oxygen while diving. Using less oxygen suggested less stress, thus proving who was least rattled under water. Mr. Ackman really, really likes to win. Continue reading the main story

“When we lost at tennis, always, on some fundamental level, he regarded it as an aberration,” recalled Michael Grossman, his tennis partner in high school.

Mr. Ackman had an upper-middle-class upbringing in the New York suburbs, and he recalls plenty of rough-and-tumble arguments at home with his parents and sister. “Let me win?” Mr. Ackman recalled. “That doesn’t exist in my house. No one lets anyone win. Fight to the death.”

And if, at times, that means putting his fund and reputation at risk, so be it.

“I think he is just prepared to live with the scrutiny and the calumny heaped upon his head,” said William A. Sahlman, one of his professors at Harvard Business School.

This year, Mr. Ackman made a rare move. It began with a meeting in early February between him and J. Michael Pearson, the chief executive of Valeant. Five days later, Mr. Pearson expressed his interest in buying Allergan, the maker of Botox, and sought Mr. Ackman’s help, according to Valeant’s regulatory filings. Mr. Ackman agreed and began buying shares in Allergan through a unique partnership with Valeant later that month, eventually building a $4 billion stake in the company. By April, Mr. Ackman and Valeant had gone public with a bid for the company worth $47 billion. It went hostile.

“A hedge fund getting together with another company to buy out a competitor?” said Alan Palmiter, a business law professor at the Wake Forest University School of Law. “That’s definitely unusual. I can’t recall ever seeing a hedge fund being part of an industry takeover.”

Allergan had stronger words for Valeant and Mr. Ackman. It rejected the deal and warned shareholders that Valeant would squeeze the company for profit and skimp on research. In a federal lawsuit, Allergan contended that the Valeant-Ackman partnership was an “improper and illicit insider-trading scheme hatched in secret by a billionaire hedge fund investor.” The S.E.C. is now investigating. Pershing Square denies the accusations.

The short-seller James S. Chanos, who predicted the fall of Enron, has called Valeant’s accounting aggressive and joined the fight — against Mr. Ackman.

While Mr. Ackman drew support from big Allergan shareholders — including T. Rowe Price and Pentwater Capital Management, and proxy advisers like Glass Lewis — for a special shareholder meeting in December to vote on a new board, the clash has intensified. In early October, Mr. Ackman provided a sometimes testy deposition for the Allergan lawsuit. (After confirming that he had given depositions “a number” of times before, Mr. Ackman added, “I love depositions.”)

Neither side shows signs of backing down ahead of the shareholder vote. In court filings, Valeant and Pershing have accused Allergan of providing false information about Valeant to shareholders. Allergan said last week that it saw no evidence to support those claims. Valeant and Pershing, meanwhile, have raised their offer twice and have signaled they might raise it again in the next few weeks, to $60 billion.

‘A Sad Performance’

For three hours on a sunny day this past July, Bill Ackman ranted. He raved. He brought up comparisons to Enron. To the Mafia. To the Nazis. He cried.

He did this in front of an audience of nearly 500 people in a Midtown Manhattan auditorium. He had billed this as the “most important” presentation of his career, promising that it would be the “death blow” against Herbalife, the nutritional supplement club that he has bet against.

It seemed to have the opposite effect. Throughout the jaw-dropping exhibition, Herbalife’s stock rose higher, ultimately closing the day up 25 percent.

The presentation was so over the top that other hedge fund investors, friends and even members of Pershing Square’s own advisory board quickly labeled it a mistake. “It was one of the few times that I felt sorry for Ackman, a guy who makes more in a day than I make in a year,” said Erik M. Gordon, a professor at the Ross School of Business at the University of Michigan. “It was a sad performance, and it was, minute by minute, calling into question his judgment and credibility.” Mr. Ackman’s theatrical sense had gone wrong; later, he told Bloomberg News that the presentation “was a P.R. failure.”

Others feared the bet itself, which at one point totaled 10 percent of Pershing’s assets. At least one investor had already redeemed his money.

“I’m sure we had some redemptions from people who were nervous about Herbalife,” Mr. Ackman said in the Pershing conference room.

The head of a firm that invests in hedge funds, speaking on condition of anonymity because he might someday invest with Mr. Ackman, said: “There are two schools of thought on Herbalife. Bill thinks this is an outright fraud that will be convicted. To take that big a bet for your fund and your investors, I think it’s foolish.”

Even before the “death blow” presentation, Mr. Ackman had restructured his bet against Herbalife. After discussions with investors and his advisory board, he reduced Pershing’s exposure by 60 percent. But he has spent $50 million just on research and legal fees for his campaign against the company.

“Some of us might be surprised by how much he ventured — how much he got into it — but I don’t think there is anybody on the board who thinks that this is now a mistake,” said Martin Peretz, one of Mr. Ackman’s professors at Harvard, who was an early investor in Gotham and serves on Pershing’s advisory board. (Members of the advisory board each received 1 percent of the firm.) That Herbalife’s share price has fallen 34 percent this year helps, he added. Still, Mr. Ackman’s position will start making money only if Herbalife stock falls roughly another 9 percent.

The Federal Trade Commission and the S.E.C. have opened inquiries into Herbalife and its practices — in no small part because Mr. Ackman lobbied regulators and lawmakers to encourage investigations. The S.E.C. is also looking at Pershing Square and some of the investors who took the other side of the bet.

Some hedge fund executives wonder whether Mr. Ackman has lost his perspective on Herbalife, allowing it to become a personal vendetta.

“I think Bill has gotten very angry about what Herbalife is doing, and the presentation made it very clear that it’s personal to him,” said Whitney Tilson, a hedge fund manager and a longtime friend of Mr. Ackman. “He wants to be vindicated for his personal reputation as well.”

Mr. Ackman argues that he maintains plenty of rational distance. When asked if he could absorb any new information that might change his thesis against Herbalife, he first nodded curtly. Certainly, yes.

But, unable to stop himself, he fell into a familiar refrain. “There’s nothing actually that could prove that Herbalife is not a pyramid scheme,” he said. “There’s nothing.”

Maybe Mr. Ackman is capable of changing his mind. Or maybe not. As for Herbalife, he finished heatedly, “That’s a bad example.”

This article provides a great profile of a well-known hedge fund titan. I track Bill Ackman's Pershing Square and many other top funds every quarter (next one will be out in a couple of weeks). Ackman's fund is having a great year, which is why he's leading the pack in 2014. But as I keep warning my readers, beware of investing in the hottest hedge funds.

As far as egos, there is no doubt Ackman has a huge ego and it often comes back to bite him in the ass, making some of his investors extremely nervous. The sad public display of hedge fund cannibalism didn't make him or Carl Icahn look good. In fact, it turned many people, especially those in the Jewish community, completely off which is why they wisely simmered down and made up.

What else does the article show us? Great investors invest with conviction and they're not afraid to take very concentrated bets. They will lose on some big bets but win on most which is why they typically outperform the S&P500 over a long period.

Ackman's fund has hit a few home runs, offsetting his big flops. Two of his biggest hits — General Growth Properties (GGP) and Canadian Pacific (CP) — helped to offset the reputational and financial losses from Target (TGT) and J. C. Penney (JCP).

I must admit, I always thought J.C. Penney was a dud and openly questioned why so many top hedge fund managers, including Soros, jumped on that bandwagon in the third quarter of 2013 (Soros cut his losses in the subsequent quarter). As far as Herbalife (HLF), I continue to steer clear from it as I never bought their products and don't have an opinion on the company. As far as Valeant Pharmaceuticals (VRX), Ackman might be right but I wouldn't bet against Jim Chanos, the man who exposed Enron as a fraud.

Bridgewater Associates LP, the $160 billion hedge-fund firm founded by Ray Dalio, sued two former employees who started competitor Convoy Investments LLC, claiming they exaggerated their previous roles with Bridgewater to win clients.

Convoy founders Howard Wang and Wenquan Wu, who Bridgewater said served in “low-ranking roles” in client services and information technology, have tried to pass themselves off as “former key figures,” according to the firm’s complaint accusing the two of violating laws against false advertising.

“Rather than promote their new venture honestly, defendants elected to trade off of Bridgewater’s hard-earned reputation,” the Westport, Connecticut-based firm said in the Oct. 21 complaint in Manhattan federal court. Wang had publicized that he personally “managed” multibillion-dollar portfolios and helped oversee the $70 billion All Weather fund, while Wu billed himself as helping oversee various “critical components” of the company’s operations systems, Bridgewater said.

After being confronted about misleading claims, Wang and Wu took down only some of their statements from Convoy’s website, and then “mysteriously” hid the bulk of the site behind a password, Bridgewater said. The Convoy founders also submitted exaggerated claims in an application for a trademark for the new firm, according to the complaint.

Ambitions Hidden

While they had agreed to disclose their post-employment plans, Wang and Wu didn’t tell the firm that they were planning to start a competitor, Bridgewater said. The men “kept their competitive ambitions hidden,” telling Bridgewater they were “traveling, ballroom dancing” or passively advising friends and family about their investments, according to the complaint.

A representative of New York-based Convoy who wouldn’t provide a name said in an e-mail that the lawsuit claims are “baseless.”

“We believe this is a case of a giant hedge fund using its weight to scare ex-employees from becoming competition, particularly because we believe our low fee and pro bono approach is disruptive to the established industry model,” the representative said.

Bridgewater is seeking damages and a court order stopping the men from allegedly engaging in false advertising.

The case is Bridgewater Associates LP v. Convoy Fund LP, 14-cv-8413, U.S. District Court, Southern District of New York (Manhattan).

I'm keeping a close eye on this case for two reasons. First, if Bridgewater is right and these former employees are misrepresenting their experience at the fund to garner assets, then kudos to Bridgewater for exposing them.

But if this isn't the case, then I give all the credit to the founding partners of Convoy Investments for standing up to the 'Bridegewater bullies' and starting a new hedge fund with much lower fees than the established industry norm. They aren't the first fund to think of drastically chopping fees and they won't be the last.

In the hedge fund world, you won't find a bigger ego than Ray Dalio even though he will vigorously deny this claiming his critics don't understand Bridgewater's unique culture and 'radical transparency.'

I'm not a critic of Ray Dalio or Bridgewater but I have raised concerns on their size and performance in the past and some of the deals they entered with public pension funds. I was one of the first in Canada to invest in Bridgewater back in 2002 and met Ray Dalio roughly ten years ago when Gordon Fyfe and I visited their office. I even confronted him on why deflation and deleveraging is the endgame, irritating him to the point where he blurted out: "Son, what's your track record?" Fyfe got a real kick out of that response.

I like Ray and think Bridgewater is a top global macro fund which produces outstanding research to back their positions. But let there be no mistake, it's Ray's shop and he rules it with an iron fist. He will claim otherwise but look at the facts. How many Bridgewater "cubs" or "tigers" are there out there? Why haven't there been more former Bridgewater employees starting up their own fund? The evidence speaks for itself and Bridgewater's reaction to this new venture sends a strong message to any of their employees thinking of starting a new fund, "We will squash you like a bug!".

There is something else that irks me a lot. All these overpaid hedge fund gurus collecting huge fees on the billions they manage have catapulted into the Forbes' list of billionaires. Dalio is now the richest person in Connecticut with an estimated net worth of $14.3 billion (do the math...when managing over $100 billion, that 2% management fee really kicks in, making Dalio obscenely rich). Kudos to him, he's come a long way since starting his fund in a small Manhattan apartment in the mid-70s.

But when a hedge fund manager's net worth is roughly 10% of the assets he manages, I start worrying that his ego will get the better part of him and whether he's spreading enough of his enormous wealth to all his employees. What else worries me? As I've stated before, that 2% management fee should be scrapped for alternative investment funds managing billions because it turns most funds into large, lazy asset gatherers (not the case for Bridgewater but this is a legitimate concern).

As always, I welcome your feedback and if Ray Dalio or Bill Ackman have anything to say, they can contact me directly (LKolivakis@gmail.com). There are a lot of egos in finance, especially in the hedge fund industry, and that's not always a bad thing. But all these overpaid hedge fund gurus owe their enormous wealth to teachers, police officers, firefighters and other public servants working hard to make an honest living. I wish they'd recognize this and publicly thank them once in a while.

Below, Daniel Posner, chief investment officer of Opportunistic Credit at Golub Capital, and Columbia University’s Fabio Savoldelli discuss how hedge funds were impacted by volatility, the recent market selloff and where Gloub Capital is finding value. They speak on “Market Makers.”

And Skybridge Capital Senior Portfolio Manager Troy Gayeski discusses the performance of hedge funds, Fed policy and his outlook for the economy on “Bloomberg Surveillance.”

The Bank of Japan shocked global financial markets on Friday by expanding its massive stimulus spending in a stark admission that economic growth and inflation have not picked up as much as expected after a sales tax hike in April.

BOJ Governor Haruhiko Kuroda portrayed the board's tightly-split decision to buy more assets as a preemptive strike to keep policy on track, rather than an admission that his plan to reflate the long moribund-economy had derailed.

But some economists wondered if pushing even more money into the financial system would be effective as long as consumer confidence continues to worsen and demand remains weak.

"It's clearly a big surprise given Kuroda's repeated insistence that policy was on track and assorted politicians have been warning about the negative side of a weak yen currency," said Sean Callow, a currency strategist at Westpac.

"We salute the BoJ for admitting that they weren't going to reach their goals on inflation or GDP, though we do note that the new policy equates to about $60 billion of quantitative easing per month. This perspective does raise the question of just how much impact monetary policy is having."

The jolt from the BOJ, which had been expected to maintain its level of asset purchases, came as the government signaled its readiness to ramp up spending to boost the economy and as the government pension fund, the world's largest, was set to increase purchases of domestic and foreign stocks.

"We decided to expand the quantitative and qualitative easing to ensure the early achievement of our price target," Kuroda told a news conference, reaffirming the BOJ's goal of pushing consumer price inflation to 2 percent next year.

"Now is a critical moment for Japan to emerge from deflation. Today's step shows our unwavering determination to end deflation."

Kuroda said the BOJ's easing was unrelated to major portfolio changes by the Government Pension Investment Fund (GPIF) also announced on Friday, but the effect of the day's two major decisions means that the central bank will step up its buying of Japanese government bonds, offsetting the giant pension fund's increased sales of them.

The BOJ's move stands in marked contrast with the Federal Reserve, which on Wednesday ended its own "quantitative easing," judging that the U.S. economy had recovered enough to dispense with the emergency flood of cash into its financial system.

In a rare split decision, the BOJ's board voted 5-4 to accelerate purchases of Japanese government bonds so that its holdings increase at an annual pace of 80 trillion yen ($723.4 billion), up by 30 trillion yen.

The central bank also said it would triple its purchases of exchange-traded funds (ETFs) and real-estate investment trusts (REITs) and buy longer-dated debt, sending Tokyo shares soaring and prompting a sharp sell-off in the yen.

Kuroda said that while the economy continues to recover, plunging oil prices, slowing global growth and weak household spending after the tax hike were weighing on price growth.

"There was a risk that despite having made steady progress, we could face a delay in eradicating the public's deflation mindset," he said.

Before Friday's shock decision, Kuroda had been relentlessly optimistic that the unprecedented monetary stimulus he unleashed 18 months ago would succeed in bolstering an economic recovery and ending 15 years of falling prices.

But the world's third-largest economy has sputtered despite the BOJ's asset purchases and earlier government spending.

Most economists polled by Reuters last week had expected the central bank to ease policy again but not so soon. A majority had expected it to move early next year.

The bank's previous failed effort to defeat deflation via quantitative easing (QE) in the five years to 2006 failed.

ECONOMY FLOUNDERING

Still, Economy Minister Akira Amari called the BOJ's easing a timely move, saying the decision was related to but separate from Prime Minister Shinzo Abe's looming decision on whether to raise the sales tax again next October, which would help rein in hefty government debt but risk a further economic blow.

In a semiannual report, the BOJ halved its growth forecast for the fiscal year to March to 0.5 percent. It trimmed its CPI forecast for fiscal 2014 and 2015, but still expects to meet its inflation target within the two years it originally set out. "This is very significant because it reasserts Kuroda's leadership over the policy board, which was beginning to show open dissent," said Jesper Koll, director of research at JPMorgan Securities.

"It recognizes what we have known, that the real economy has been weaker than expected, weaker than forecast, and reasserts that Kuroda thinks they can do something about this."

The benchmark Nikkei stock index .N225 spiked to a 7-year high on the BOJ bombshell and closed up 4.8 percent. The yen tumbled, with the dollar climbing to 110.91 yen, its highest since 2008, from 109.34 before the announcement.

"It’s easy money, so financials, banks and securities, and real estate stocks stand to benefit further," said Masayuki Doshida, senior market analyst at Rakuten Securities.

In a reminder of the challenges the central bank faces, data earlier on Friday showed annual core consumer inflation was 1 percent when stripping out the effect of April's tax hike, half the BOJ's target.

Household spending fell for a six straight month in September from a year earlier, while the job-availability rate eased from its 22-year high in August.

Also on Friday, a Japanese government panel overseeing the GPIF approved plans for the fund to raise its holding of domestic stocks to 25 percent of its portfolio from the current 12 percent.

The $1.2-trillion GPIF is under pressure from Abe to shift funds towards riskier, higher-yielding investments to support the fast-ageing population, and away from low-yielding JGBs.

With Abe set to decide in December whether to raise the sales tax next year to 10 percent from 8 percent, voices are growing for him to delay the planned fiscal tightening, given the economy's weakness.

Isamu Ueda, a senior official in Komeito, the junior party in Abe's coalition, said on Friday it would be difficult to press ahead with plans to raise the tax next year.

"I think conditions are severe for (raising the tax) next October," Ueda told reporters after a meeting of Komeito's economic revival council, which he heads.

The surprise decision by the Bank of Japan to engage in more quantitative easing prompted a huge rally in global equities and at this writing, U.S. stock futures are up sharply.

So what is going on? Despite unprecedented monetary and fiscal stimulus, Japan is still trying to slay its deflation dragon and Europe and the United States better be paying attention because this could very well be their future.

Interestingly, the Fed ended its quantitative easing program a couple of days ago and if you read the FOMC statement, it was somewhat hawkish, which makes me wonder if the Fed is on track for making a huge policy blunder.

Importantly, I think the Bank of Japan is right to be worried and the Fed is too complacent about contagion risks emanating from the euro deflation crisis, taking away the punch bowl too soon. The doves on the Fed, like James Bullard, understand the dangers of deflation spreading to the U.S. and why it's important to leave the door open for more QE down the road, but he's not a voting member. Charles Plosser and Richard Fisher, two of the hawkish presidents on the FOMC, voted to end QE but they will be replacedearly next year and this could change the tenor of debate within the U.S. central bank's policy-setting committee.

...the biggest policy mistake the hawks on the FOMC are making is ignoring global weakness, especially eurozone's weakness, thinking the U.S. domestic economy can withstand any price shock out of Europe. If eurozone and U.S. inflation expectations keep dropping, the Fed will have no choice but to engage in more QE. And if it doesn't, and deflation settles in and markets perceive the Fed as being behind the deflation curve, then there is a real risk of a crisis in confidence which Michael Gayed is warning about. Perhaps this is the real reason why big U.S. banks are loading up on bonds (not just regulatory reasons).

It's also interesting to read how Japan's giant pension fund, the GPIF, is unloading JGBs to buy domestic equities but the BoJ is snapping them up to keep rates low (central banks are more powerful than giant pension funds). What does all this mean for the markets? Global risk assets will continue to rally and we will await the news from the European Central Bank to see if it finally starts engaging in massive QE. Morgan Stanley and Goldman Sachs are warning that European QE, while fully priced in, is neither imminent nor likely. If that's the case, then expect the Fed to stand ready to engage in more QE down the road, especially if inflation expectations keep dropping despite massive global monetary stimulus. Former Federal Reserve Chairman Alan Greenspan is right to warn of market turmoil as QE unwinds, but I don't think he understands the real danger in the global economy, namely, a protracted period of debt deflation. BoJ Governor Kuroda is way ahead of his global counterparts but he's fighting a losing battle. No matter what monetary authorities do, deflation and deleveraging are coming, and that will scare everyone next Halloween. Below, Marc Lasry, Avenue Capital chairman & CEO, explains how his hedge fund was able to profit from banks and Europe's "structural issues." Lasry also explains why he likes energy plays now, but he prefers playing the credit side than investing in energy stocks (I wouldn't touch energy or commodity stocks until you get a better sense of where inflation expectations are heading).

One thing Lasry said that I really liked (not in clips below) was when the risk-free rate was at 4%, distressed debt investing was expected to deliver 20% annually (5x the risk-free rate) but with rates at 0.25%, investors are happy with low to mid-teen returns, recognizing the "risk parameters have changed" and you have to take on a lot more leverage to obtain these returns. Smart guy which is why he's one of the best distressed debt investors in the world. Happy Halloween, enjoy your weekend.

“Be very, very careful what you put into that head, because you will never, ever get it out.”

— Cardinal Thomas Wolsey on King Henry VIII

So it is with inflation. A generation of economists and central bankers who lived through the 1970s learned that there is a large risk from runaway inflation and that steps must be taken to stop it before it gets out of control.

In reality, the threat these days comes from inflation that is too low, or even from deflation. Many of the world’s economic problems would be reduced if we could get more inflation than we have now.

Unfortunately, some central banks concluded after the first bit of revival from the Great Recession that it was time to tighten credit, lest super low interest rates bring a burst of inflation pressure. They saw a need to confront the possibility of soaring prices before it was too late.

The Swedish central bank, which began to raise interest rates in 2010, in part because of worries about a housing price bubble, completed its reversal of policy on Tuesday, cutting its target interest rate to zero after raising it as high as 2 percent in 2011. But Lars E. O. Svensson, a noted economist who resigned from the Swedish central bank board last year, warned that more steps might be needed, including negative interest rates.

The Swedish blunder was not as great as the one committed by the European Central Bank when it raised rates in 2008 — a worse time to do that is hard to imagine — and then again in 2011. Mario Draghi, who became E.C.B. president in late 2011, has done yeoman work to offset the damage of that policy, but consumer price indexes in several eurozone countries are indicating deflation has arrived.

On Wednesday, the Federal Reserve’s Federal Open Market Committee sort of ended its program of buying long-term Treasury bonds and mortgage-backed securities, known as Q.E. for quantitative easing. But it will not unwind those purchases, at least for the time being. As the securities it owns mature, the Fed will roll over the proceeds into new securities.

Now, with quantitative easing ending, what has the Fed accomplished?

It has helped the economy, although not nearly to the extent that might have been hoped. Inflation, far from accelerating as some conservative economists forecast, has been running consistently below the Fed’s 2 percent target. The Fed’s preferred measure, the index of personal consumption expenditures, is up 1.5 percent over the last 12 months, both overall and excluding volatile food and energy prices. It has been more than two years since either measure was up as much as 2 percent. Imagine the criticism hurled at the Fed if inflation had been running above its target for that long.

What we have not heard from the Fed is any clarification of what it will do if inflation does not pick up, let alone if it falls close to or below zero.

“The real question,” said Jon Faust, an economist at Johns Hopkins University, “is how the F.O.M.C. will express its commitment to getting inflation back to 2 percent.” Until he left the Fed this summer, he was a special adviser to the last two Fed leaders, Ben Bernanke and Janet Yellen.

Mr. Faust was speaking before the Fed’s statement on Wednesday. The answer was that the Fed did not have many words about the question, let alone the “words with teeth” that Mr. Faust believes are likely to become appropriate.

The only dissent at Wednesday’s meeting came from Narayana Kocherlakota, the president of the Federal Reserve Bank of Minneapolis, who in a speech this month said, “In my view, inflation below 2 percent is just as much of a problem as inflation above 2 percent.” He wanted a commitment to push inflation up to 2 percent.

“The likelihood of inflation running persistently below 2 percent has diminished somewhat since early this year” was all the Fed statement had to say about the issue.

There is nothing magic about 2 percent, and some economists think that a 3 or 4 percent target might make more sense. But you don’t have to favor a higher target to realize the current inflation rate is not helping the economy.

At the moment, the threat of deflation is clearly greater in Europe than it is in the United States, and presumably some of the factors forcing prices down, including falling agricultural commodity and energy prices and a strengthening dollar, will diminish as time goes on. But if those weakening commodity prices signal a coming decline in economic activity around the world, the picture could worsen.

What is needed is for Fed officials, and other economists, to make clear some of the damage that low inflation can inflict on an economy. They make adjustments harder for countries that need to become more competitive. Cutting nominal wages is difficult and can be devastating for workers facing fixed costs, like mortgage expenses. But if there is inflation, real wages can decline as nominal wages remain level.

It has become common for some economists to denounce the effect of low interest rates on fixed-income investors, but that is not the complete story. Certainly those with money to invest now face an unappealing set of choices. But those who bought long-term securities years ago — when inflation was expected to be considerably higher than it now is — are receiving more value than they expected.

The much discussed ratio of national debt to gross domestic product also suffers. Consider the 18 nations in the eurozone. Collectively, their national debts rose by 7.8 percent in 2012 and 2013, forcing up the debt-to-G.D.P. ratio by 5.2 percentage points. From 2004 to 2006, their debts rose nearly as rapidly, by 7.4 percent. But the debt-to-G.D.P. ratio actually fell by a percentage point. At the time, European economies were growing and inflation was also pushing up the nominal gross domestic product figures. Now there is little if any growth or inflation, and the result is to worsen the debt picture.

The markets inferred from the Fed’s statement that credit tightening through higher interest rates would more likely arrive sooner than expected, and the dollar rose. If the economic growth and job figures continue to look good, and if inflation manages to rise at least a little, that forecast could be a good one.

But what will happen if inflation — and inflation expectations — do decline? So far, as can be seen in the Survey of Professional Forecasters conducted quarterly by the Federal Reserve Bank of Philadelphia, the 10-year inflation forecast has remained stable at 2 percent. If it began to fall, that would catch the attention of Fed officials.

But the bond market is not so confident. The market inflation forecast can be estimated by calculating the inflation rate at which a purchase of a normal Treasury security would be no better or worse than the purchase of an inflation-protected Treasury security of the same maturity. At the end of last year, the 10-year inflation forecast was 2.2 percent; now it is 1.9 percent. The one-year forecast then was 1.5 percent; now it is a forecast of deflation, negative 0.75 percent.

What could the Fed do if it turns out deflation is a real threat? In theory, it could resume quantitative easing. It could also jawbone Congress to provide more fiscal stimulus. If the Republicans win control of the Senate in next week’s elections, the first alternative might bring angry denunciations from both sides of Capitol Hill. The second might simply be ignored.

As long as deflation is a possibility, the Fed would be well advised to explain, again and again, why inflation that is too low is also bad for the economy. The lesson that high inflation is a threat is well known to politicians and voters. There is a need, as Cardinal Wolsey might have said, to get something else into their heads.

Correction: November 1, 2014

The High & Low Finance column on Friday, about the risks of deflation, misstated the market forecast for the 10-year inflation rate. It is 1.9 percent, not 1.7 percent.

Deflation isn't really a "new" risk. It's been a key theme on this blog for as long as I can remember because I've been worried about it from the time I went head to head with Ray Dalio at Bridgewater back in 2004. I was even more worried after researching structured credit markets in the summer of 2006, looking closely at how CDOs-squared and cubed were being (mis)used to fan the flames of the U.S. housing bubble.

Interestingly, the Fed ended its quantitative easing program a couple of days ago and if you read the FOMC statement, it was somewhat hawkish, which makes me wonder if the Fed is on track for making a huge policy blunder.

Importantly, I think the Bank of Japan is right to be worried and the Fed is too complacent about contagion risks emanating from the euro deflation crisis, taking away the punch bowl too soon. The doves on the Fed, like James Bullard, understand the dangers of deflation spreading to the U.S. and why it's important to leave the door open for more QE down the road, but he's not a voting member. Charles Plosser and Richard Fisher, two of the hawkish presidents on the FOMC, voted to end QE but they will be replacedearly next year and this could change the tenor of debate within the U.S. central bank's policy-setting committee.

...the biggest policy mistake the hawks on the FOMC are making is ignoring global weakness, especially eurozone's weakness, thinking the U.S. domestic economy can withstand any price shock out of Europe. If eurozone and U.S. inflation expectations keep dropping, the Fed will have no choice but to engage in more QE. And if it doesn't, and deflation settles in and markets perceive the Fed as being behind the deflation curve, then there is a real risk of a crisis in confidence which Michael Gayed is warning about. Perhaps this is the real reason why big U.S. banks are loading up on bonds (not just regulatory reasons).

The BoJ's surprise also reinforced the trend in the mighty greenback, sending the U.S. dollar soaring against both the yen and the euro. This too is very important because a significant bullish multi-year trend in the U.S. dollar has huge implications on asset allocation decisions, many of which most pension funds and corporations are ill-prepared for.

Ironically, the surge is the U.S. dollar is disinflationary and potentially deflationary because it lowers import prices. It also acts as an interest rate increase, tightening U.S. financial conditions. Hence, even though the Fed ended QE and isn't going to raise rates anytime soon, financial conditions are already tightening in the United States via the soaring greenback.

Filling up the car with diesel the other week, I was pleased to discover something which – at least for someone of my generation – still feels very unusual; the price had gone down – again. And it’s not just fuel. It’s food, it’s clothing, it’s laptops, it’s air fares and much else. Indeed, were it not for the ever mounting costs associated with housing, including rents and utility bills, the CPI inflation rate for the UK last month would have been just 0.8 per cent. The picture for shop prices looks even more dramatic; according to the British Retail Consortium, non food price deflation on the high street accelerated to 3.2 per cent in September.

For those of us who spent our formative years in the inflationary 1970s and 1980s, this is an unfamiliar, even alien world. Back then, the big economic challenge was double-digit inflation, which Britain in particular seemed perennially prone to. Interest rates were repeatedly raised and lowered to cope, entrenching a pattern of economic boom and bust that was devastating for industry. It was not until the Great Moderation of the Nineties and early Noughties that the UK was able to kick the habit.

Today the threat is very different and, many would argue, very much more serious – that of stubbornly persistent economic stagnation and price deflation. That we are still worrying about this a full six years after the start of the financial crisis is itself something of an eye opener. Trillions of dollars worth of central bank money printing was meant to have seen off the spectre of deflation once and for all. Regrettably, it has not.

In Sweden this week, the Riksbank imposed a negative interest rate in a belated attempt to address what is now a virtually two-year stretch of falling prices. At least six of the eurozone economies are in price deflation. To that list can also be added Europe’s second largest economy, France, if the impact of increases in sales taxes is excluded.

Even for economies which are growing again, such as the UK and the US, the picture is not good. Analysis by the investment bank Jefferies shows that the proportion of the US inflation basket where price increases are below 1 per cent is at an all-time high. Similarly, the proportion where the inflation rate is above 3 per cent is at an all-time low. Some 31 per cent of the prices that make up “core” US inflation – that is stripping out shelter, food and energy – are now in outright deflation.

If these phenomena were predicted, it might not seem quite so worrying. Presumably, timely action would already have been taken. Yet the fact is that the US Federal Reserve, the Bank of England and the European Central Bank all find themselves continually wrong-footed in their forecasts of the downward pressure on prices. Despite record low interest rates and the wholesale application of squillions in quantitative easing, all three central banks are struggling to make inflation meet mandated targets. If even growing economies can’t restore equilibrium, what hope the eurozone, where years, if not decades, of low inflation or even outright deflation are fast becoming a virtual certainty?

Economists used to talk about the risks of “Japanification” for Europe. The way things are going, this assessment ought perhaps to be reversed; is there any hope of Europe actually avoiding it? It’s hard to imagine that good old inflationary Britain would ever succumb to this trap, yet in terms of wages, we already have. Not since the 1870s have real wages seen such prolonged and deep erosion. And if the eurozone does fall into outright price deflation, it will undoubtedly drag us down with it. Britain cannot forever remain Europe’s debt-fuelled consumer of last resort.

What’s all the fuss about, some ask? Falling prices – that’s surely a good thing? For those with secure forms of fixed income, it most certainly is; it makes them better off. It is also undoubtedly true that there are “good” forms of deflation, created generally speaking by bountiful, and growing, supply. We can include falling commodity, food and energy prices in this category. When these basics fall in price, it puts money in people’s pockets for spending on other things.

It was this type of “good” deflation that characterised much of the Industrial Revolution, and to a lesser extent the 1920s, when there were productivity-enhancing breakthroughs in the application of technology that massively expanded supply. Prices dropped, but consumption, living standards and output boomed.

Admittedly, there are elements of this type of deflation in present pricing pressures. Since the 1960s, the price of a unit of computing power as measured by Floating Point Operations Per Second (Flops), has fallen from an astonishing $8.3 trillion in today’s money to little more than 10 cents. These gains have driven major gains in productivity and substantially changed the nature of work, growth and output.

Yet unfortunately they are probably a comparatively minor part of today's deflationary story. Current deflationary pressures seem substantially to be made up of the “bad” variety, particularly in the eurozone – the kind that stem from financial crises, deep recessions, and big debt overhangs, where demand is depressed below the level of supply. The reason why bad deflation is not a disease you ever want to succumb to, and why central bankers spend so much time obsessing over it, is that once entrenched, it’s very hard to get rid of. Inflation can easily be tamed simply by bearing down on demand with higher interest rates. Lifting demand is far more problematic, however, and once rates reach the zero bound, seemingly well nigh impossible.

If prices are falling, consumers postpone spending decisions in anticipation of getting a better deal tomorrow, and instead save more. This depresses demand, causing companies invest less, employ less, and pay less. Soon a vicious cycle of declining demand establishes itself, made worse by any sizeable debt overhang, the burden of which grows as real wages shrink, making people even more averse to spending.

Sometimes both “good” and “bad” deflation are present, as in today’s falling supermarket prices. The “good” comes from the price war unleashed by the discounters, Aldi and Lidl among them. The “bad” comes from the fact that falling real wages has depressed demand. Consumers have to make less go further.

Yet even accepting that today’s deflationary pressures are substantially demand led, or “bad”, in nature, it is not clear that ever more extreme forms of monetary activism are the answer. There is a good reason why central bankers are desperate to wean their economies off the adrenalin fix of quantitative easing, and why the Federal Reserve for one is so relieved to have brought its programme of asset purchases to a conclusion this week: if it ever did work, it’s self evidently not doing so any longer.

By creating new asset bubbles, sowing the seeds for future financial instability, and widening the wealth divide, it’s also been generating some very undesirable side effects. Monetary activism may have helped save the UK and the US from greater calamity after the financial crisis, but it only steals growth from the future and from others. One effect of loose money is currency devaluation, which might give a temporary boost but merely shifts the deflationary problem onto other states. This in turn produces a race to the bottom as each country attempts to outdo the other. Globally, it’s a zero sum game. Fiscal stimulus and credit expansion have also been tried, and so far succeeded only in sending national debt levels skyrocketing, for no lasting effect in terms of growth.

In my view, all these approaches are based on a fundamental misunderstanding of what the crisis is all about. The downturn was never just some cyclical aberration that could be easily overcome via traditional monetary and fiscal demand management. Rather, it was a manifestation of deep structural problems – excessive debt in some areas; excessive saving in areas – both within and between national economies.

Until these structural imbalances and supply-side deficiencies – such as the UK’s pitifully inadequate levels of housebuilding – are addressed at national and international level, low inflation and becalmed living standards may be about the best we can look forward to.

Jeremy Warner is right, there are deep structural factors reinforcing the deflationary trend we're witnessing across the world, and all the monetary and fiscal stimulus won't stop or reverse it.

Central banks are fighting a losing battle and their attempts to reflate risk assets will only deepen the wealth divide, which in and of itself is also deflationary (how long can the top 10% of households prop up the recovery?). Worse still, more quantitative easing is sowing the seeds of another huge crisis which will eventually hit everyone hard.

But central banks don't have much of choice. If they stand idle, deflation will set in, making their job to achieve their inflation target that much more impossible. And they can't count on politicians to promote pro-growth policies because dysfunctional politics and fiscal austerity are pretty much the new norm everywhere nowadays.

People don't understand deflation. They think it's all rosy but it isn't. I just visited the epicenter of the euro crisis in September and saw firsthand the ravages of deflation. Significantly lower wages, pensions and real estate values are wreaking havoc on the Greek economy. The same thing is going on in Spain, Italy and Portugal and France will soon follow.

This represents a significant and protracted price shock that can spread throughout the world. The main focus now is on the U.S. recovery and better employment but if the Fed doesn't keep its eye on the euro deflation crisis and contagion risks, it will be making a terrible policy blunder. And I think markets are extremely nervous about the Fed and the ECB falling behind the deflation curve (more the Fed because most people have given up on the ECB engaging in massive quantitative easing).

What else worries me? I think policymakers and economists are overestimating the strength of the U.S. economy, which is still sending mixed signals at best. There is a recovery going on but it's a slow, grinding recovery and the quality of the jobs being created are nowhere near as good as in past booms. It's even worse in Canada, where I fear complacency is leaving Canadians ill-prepared for the storm ahead.

I'm sorry I couldn't be more cheerful but I think a lot of institutional investors are going to get clobbered in the years ahead because they underestimated the risks of deflation spreading to North America. For now, it's "only a European problem," much like the Germans were saying about Greece ("it's only a Greek problem"). Yeah right, keep hoping, but that's not a strategy.

Below, CNBC reports that bond investing guru Bill Gross is warning that deflation remains a growing possibility despite aggressive monetary policies by central banks around the world. In his second investment outlook letter since quitting Pimco, the bond firm he co-founded more than four decades ago, to join Janus Capital Group in September, Gross said history shows that economies experience periods of both inflation and deflation, and both "are the enemies of stability and growth."

Also, on Friday, Brian Kelly was on CNBC and likened the BoJ's Halloween surprise to a Bear Stearns event."What they did is outrageous. It is a terrible idea," he said. "It is going to have massive, massive ramifications. The U.S. stock market hasn't woken up to it yet, but they absolutely will. First thing that's going to happen is we're going to get deflation over here in the U.S."

He's wrong castigating the Bank of Japan for engaging in more QE but right on one thing, deflation will eventually come to the United States and far too many investors are grossly ill-prepared for it.

The U.S. Securities and Exchange Commission is examining how private equity firms report a key metric of their past performance when they market new funds to investors, as the regulator boosts its scrutiny of the industry, according to people familiar with the matter.

At issue is how private equity firms report how they calculate average net returns in past funds in their marketing materials, the sources said.

Net returns, also known as the net internal rate of return (IRR) and an indicator of investors' actual profits, deduct private equity fund investors' fees and expenses from a fund's gross profits. Private equity fees are not standard and different investors in the same fund can pay different fees.

Fund investors such as pension funds, insurance companies and wealthy individuals – known as limited partners - pay the fees to the private equity firm. The private equity firm and its managers, called general partners, also typically invest some of their own money into the funds, but don't pay any fees.

Including the general partner's money in the average net returns can inflate the fund's average net performance figure, and the SEC is investigating whether private equity fund managers properly disclose whether they are doing that or not, the sources said.

A SEC spokeswoman declined to comment.

The SEC's focus on the average net IRR disclosures, which has not been previously reported, marks a new phase in the agency's efforts to regulate private equity and comes at a time when the industry is already under pressure from investors to simplify its fees and expenses structure.

The emphasis on performance figures is likely to cause many buyout firms to review their regulatory compliance measures and force them to increase disclosures and make their numbers more intelligible to investors.There is no standard practice for calculating average net IRRs among the roughly 3,300 private equity firms headquartered in the United States.

A Reuters review of regulatory filings and interviews with people familiar with different firms' practices show the calculation varies widely even among the top private equity firms.

Blackstone Group LP, Carlyle Group LP and Bain Capital LLC, for example, do not include money that comes from general partners in average net IRR calculations, while Apollo Global Management LLC does, the review shows.

Fund marketing documents are not public, but the sources said all these firms disclose to investors whether they include general partner capital in the calculation or not.

The SEC's review comes after the agency put together a dedicated group earlier this year to examine private equity and hedge funds that had to register with it as part of the 2010 Dodd-Frank financial reform law, Reuters first reported in April.

Much of the SEC's focus so far had been on fees that private equity funds charge. In a May 6 speech, Andrew J. Bowden, director of the SEC's Office of Compliance Inspections and Examinations, said more than half of the private equity funds the agency examined had inappropriately allocated expenses and collected fees. COMPLEX CALCULATION

The average net IRR figure is crucial to investors' understanding of their actual profits from private equity funds. That's because not all investors in a fund pay the same amount of fees to the private equity firm for managing their money.

Typically, fund managers charge a management fee of about 1.5 percent of committed capital and take 20 percent of the fund's profits assuming performance meets a returns hurdle agreed with investors.

Investors, however, are usually offered fee breaks if, for example, they commit money early during the fundraising process or if they make a larger allocation to the fund.

The SEC expects private equity firms to report average net IRRs alongside gross IRRs with equal prominence in marketing materials when they are seeking to raise a new fund.

Industry sources said including general partner capital in the average net IRR calculation can make a material difference if that commitment is sizeable.

"Over the past five years, some general partners have started to invest more of their personal capital into their vehicles on a non-fee basis and that obviously can create some IRR distortion," said David Fann, chief executive officer of TorreyCove Capital Partners LLC, a private equity advisory firm.

I'm glad the SEC is finally scrutinizing the performance figures of the private equity industry to shine some light on whether these figures are exaggerating net returns.

Admittedly, the inclusion of a general partner's money is not a big deal in the smaller funds but large public pension funds and sovereign wealth funds typically invest in large well-known buyout funds, and they invest big sums alongside their investors.

As the article states, including the general partner's money in the average net returns can inflate the fund's average net performance figure, and the SEC is investigating whether private equity fund managers properly disclose whether they are doing that or not.

In her comment, Yves Smith (aka Susan Webber) notes the following:

We’ll put aside an issue that we’ve discussed at some length in past posts, that IRR is a terrible way to measure returns. As McKinsey put it,”…typical IRR calculations build in reinvestment assumptions that make bad projects look better and good ones look great.”

As far as the SEC investigation is concerned, there are actually two issues here, and the SEC is focusing on the worst of the two. One is, as the article notes, is that the some funds are basing their return calculations with general partner capital included, and since the general partners don’t pay any fees, including their funds in the return calculation has the effect of increasing it.

There’s a second issue, and it’s surprising the SEC hasn’t taken interest in it (or maybe it is but hasn’t figured out what to do about it) is that even the use of an “average net returns” will exaggerate prospective returns for many investors, meaning pretty much all the smaller ones. For instance, investors have succeeded in negotiating reductions in fees many general partners charge, the so-called monitoring fees (annual consulting fees charged to portfolio companies) and transaction fees (which are basically double-dipping, since these general partners hire investment bankers who charge merger & acquisition and financing fees of their own). These reductions come in the form of rebates credited against the annual management fees. These rebates typically range from 60% to 100%, with 80% considered to be a representative level. Industry leader CalPERS generally gets a 100% rebate.

The question is whether a small or newbie investor, who is likely to get only a 60% rebate, has the acumen to adjust the “average net IRR” he is presented in his marketing materials to a level to what someone like him would get on a net basis. Note that the magnitude of these fee differentials, and the lack of transparency surrounding fee differences, has turned into a full-blown row in the UK, where limited partners are less captured than in the US.

Indeed, in the UK, private equity investors are lukewarm on the asset class and they're much more vigilant on monitoring hidden fees and ensuring a level playing field for all investors, big and small.

It's worth noting, however, most of the large well-known funds do not include the general partner's money in their calculations of average net returns, but some do. The article specifically mentions Apollo Global Management (APO), which ironically has CalPERS as a huge equity owner (close to a 15% stake) and a big investor in their funds too.

As you can see below, the common shares of Apollo Global Management (APO) have had a miserable 2014, down over 30% (click on image):

The shares of other alternative investment funds have been hit too, but not to the extent of Apollo, which makes me wonder how CalPERS is fairing with this investment.