The words “bold” and “pension fund” don’t always go together easily. Then again, neither do bold and Canada.

But Canadian public pension funds are once again employing bold strategies in a world where interest rates have remained persistently low at the very moment that aging baby boomers are increasingly drawing down their retirement funds.

With traditionally safe pension investments such as bonds no longer yielding enough to cover obligations, a number of Canadian plans are ramping up leverage strategies -- approaches intended to squeeze more profit from their investments by doubling down with debt. They are mortgaging some of their swankiest skyscrapers and forming in-house hedge funds that invest in complex derivatives like forwards, swaps and options, accepting more risk in an effort to keep their promises to retirees.

"We have to earn that return somehow," said Jim Keohane, chief executive of the Healthcare of Ontario Pension Plan, which has been among the most aggressive pursuing the new leveraged strategies. "If I don’t do this, what am I going to do instead?"

It’s not the first time the Canadian funds have pushed the envelope internationally. As early as the 1990s some began establishing private equity arms to take active stakes in businesses, successfully competing with Wall Street giants for such assets as department stores, highways and, recently, pieces of GE Capital.

Hero, Goat

Today, at least seven of Canada’s large pensions have "substantial" in-house hedge fund operations. By comparison, none do in the U.S. and only two do in Europe, according to data from the international pension fund consultancy CEM Benchmarking Inc. CEM, based in Toronto, declined to name the funds, but did say the five that have been at it the longest have beaten their benchmarks by an average of 0.9 percent annually over the last five years while the 10 largest U.S. funds have managed no extra return.

“In a world where safe investments provide unacceptably low returns, they have to move farther out the risk spectrum to get the kinds of returns they need,” said Malcolm Hamilton, a retired pension fund actuary who’s now a senior fellow at Toronto’s C.D. Howe Institute. “At the end of the day, you turn out being a hero or a goat, and there’s not much room in between.”

Poaching Talent

U.S. pension funds have generally addressed the same pressures by retaining the services of Wall Street hedge funds, CEM data shows, but high fees can eat away at gains.

Unlike in Canada, where professional boards tend to oversee public funds, in the U.S. the responsibility lies with elected officials who are hesitant to approve the compensation needed to attract Wall Street talent, according to Tsvetan Beloreshki, a New York-based pension fund consultant at FTI Consulting.

Canada’s public pensions, in contrast, have been poaching top talent off Wall Street for some time. The ranks at the Canada Pension Plan Investment Board, which manages the nation’s primary public retirement fund, includes veterans from hedge fund Golden Tree Asset Management and private equity giant Carlyle Group, as well as investment banks such as Morgan Stanley, JPMorgan Chase & Co. and Goldman Sachs Group Inc., according to the CPPIB website.

Derivatives Magnify

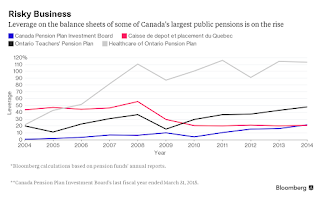

Don Raymond was recruited from Goldman to head up CPPIB’s public markets investments in 2001 and later began luring former colleagues from Wall Street as he set up an in-house hedge fund operation. At the time, leverage on CPPIB’s balance sheet -- measured as the difference between total assets and net assets -- was less than one percent. By 2011 it stood at 10 percent and by the end of the fiscal year, it had grown to 22 percent, according to publicly available data compiled by Bloomberg.

CPPIB returned 18.3 percent its fiscal year ended March 31 and had C$264.6 billion ($199.2 billion) of assets under management.

“I wouldn’t advise people to follow the Canadian path just because it seems easy; it’s actually not” said Raymond, who departed last year for Alignvest Investment Management. "If things do go wrong in derivatives, they tend to happen a lot faster than unlevered portfolios. A derivative will magnify things."

Skill Sets

Leverage at Healthcare of Ontario Pension Plan, widely known as HOOPP, now exceeds 100 percent of its net assets, leading to a more than doubling of the total assets at its disposal to invest. Ontario Teachers’ Pension Plan, the nation’s third largest, has leverage equal to half its net assets.

HOOPP earned 17.7 percent in 2014 while Ontario Teachers’ returned 11.8 percent. The Standard & Poor’s/TSX Composite Index, Canada’s benchmark equity gauge, returned 10.5 percent in 2014, including dividends.

“Traditional skill sets in pension funds are much different than what we have,” said HOOPP’s Keohane. “A lot of what we do is more like what you would see in a hedge fund.”

Asked about the leverage on its balance sheet, a spokesman for Ontario Teachers’ said derivatives are a better way to invest in certain assets. A spokesman for CPPIB said its leverage is a form of cash management that keeps the fund “nimble” and boosts returns.

Fund Firepower

In the case of HOOPP, Keohane said the fund needs to earn 3.4 percent above inflation to cover its pension obligations, no small feat given 10-year Canadian government bonds yield half that, U.S. ones are at about 2.3 percent and yields on $1.9 trillion of European debt are actually below zero. “So what we’re trying to do is find things that add incremental return with the least amount of risk,” he said.

The fact derivatives, unlike equities, can eventually expire and provide a payout means that risks from leveraging can be contained by investors with the means to ride out any interim storms, Keohane said. “We have an advantage over hedge funds because we have a balance sheet they don’t,” he said. “Nobody’s going to shake us out of a trade.”

Caisse StudyIn 2009, I covered the Caisse's $40 billion train wreck and how the media has completely covered up the ABCP scandal. There were poor decisions that took place at the highest level of the organization and it had nothing to do with derivatives but with greed and beating a ridiculous benchmark by taking the dumbest possible risks.

Yet that’s precisely what happened in the financial crisis to Caisse de depot et placement du Quebec, Canada’s second largest pension plan. The Caisse suffered a 25 percent loss in 2008 following a collapse in Canada’s market for bonds backed by short term corporate loans.

Those losses were compounded by leverage that had grown to 56 percent of assets, according to Roland Lescure, the fund’s current chief investment officer, who joined in a management shake-up made after the crisis.

"Suddenly, a book of derivatives that was not supposed to carry any directional risk started carrying some," he said. The Caisse has since brought its leverage down to about 20 percent of assets, mostly mortgages on its properties.

Proponents of today’s hedge fund strategies say the Caisse’s 2008 failure didn’t occur from using derivatives themselves, but from devoting too much money to a single market, which happened to freeze up.

C.D. Howe’s Hamilton is understanding of the new strategies but, recalling the financial crisis, still uneasy. "I’m sure there are a lot of banks who thought they knew exactly what they were doing, and they had the risks all covered off -- until they didn’t."

That's why Michael Sabia was brought in to clean up the place and he has done a very good job, more or less. Roland Lescure is a very sensible and smart CIO who isn't a cowboy and sticks to delivering solid results without taking undue risk.

The Caisse wasn't the only one taking stupid risks back then. In a clear case of abuse of derivatives, PSP was using its AAA balance sheet to sell credit default swaps, something independent financial analyst Diane Urquhart discussed on my blog. This was on top of buying ABCP, albeit not to the scale of the Caisse. All this led to PSP's disastrous fiscal 2009 results (again, senior managers didn't take my warnings seriously back then and it ended up costing me my job).

As far as Ontario Teachers' Pension Plan (OTPP) and the Healthcare of Ontario Pension Plan (HOOPP), they're in another league when it comes to internal alpha generation which is why they're the two best pension plans in Canada and the world. You can read more on Teachers' 2014 results here and HOOPP's 2014 results here.

Both these pension plans are fully funded, manage their assets and liabilities very closely, and they use derivatives extensively to intelligently leverage up their respective portfolios. Jim Keohane, HOOPP's president, has always told me that their use of derivatives is done in a way that reduces overall risk. And to be sure, their long investment horizon allows them to take derivative bets that hedge funds can only dream of (like the S&P put strategy which helped them generate huge returns in 2012).

As far as Ontario Teachers', it allocates risk internally and if it can't, it will allocate risk to the world's best hedge funds and squeeze them hard on fees (OTPP is much larger than HOOPP which is why it can't do it all internally). The folks at Teachers' also use derivatives extensively to "juice" their returns but again, we're not talking crazy risk here, more like intelligent risk taking behavior where they can capitalize on their large balance sheet and long investment horizon.

Teachers, HOOPP, the Caisse, CPPIB and all of Canada's large pensions are also doing direct investments in private equity, real estate and infrastructure, all of which are long-term, illiquid asset classes. In the last few years, most of the value added generated by these funds has come from these asset classes where they can scale up more easily.

This is one reason why Canada's pension fund was able to knock it out of the park in fiscal 2015. CPPIB is attracting talent from Wall Street, and buying it by bringing good things to life, but I take all this nonsense on poaching talent away from the Street with a shaker of salt. The top guys at Canada's large pensions get paid extremely well but let's not kid each other, even their comp doesn't match that of a top trader at Goldman or an elite hedge fund or what a managing partner of a big private equity fund receives in compensation.

[In a private meeting, Mark Wiseman, president of CPPIB, once told me: "If I could afford to hire David Bonderman I would but I can't, so unlike infrastructure where we invest directly, in private equity, we will always invest and co-invest with top funds." But the GE deal proves that CPPIB can also go out and buy talent if it wants to invest in certain segments of private equity directly.]

Now, you might read this and think why can't U.S. public pension funds do the same thing as their Canadian counterparts? The answer: lack of proper pension governance. U.S. public pensions are plagued by too much political interference and that's why they will never pay their pension fund managers properly to bring assets internally. It's not that they don't have smart people, they do, it's that the entire investment process has been hijacked by consultants which pretty much shove everyone in the same high fee brand name funds.

I had a very long day, was at a conference all morning meeting with real estate, private equity and VC funds in "speed dating" session that was fun but it drained me (thank god I never tried speed dating for real!).

Below, once again, Nicole Musicco, Managing Director for Asia-Pacific and head of the Hong Kong office of the Ontario Teachers' Pension Plan, discusses the fund's portfolio diversification. Listen to her comments and you'll understand why the world's pension fund heroes are working at large Canadian pensions. And take all this stuff on Canada's highly leveraged pensions with a grain of salt!