CBC News has learned Prime Minister Mark Carney has invited 100 of the world's biggest investors to a summit in Toronto this September. The conference aims to pitch organizations that control trillions of dollars in capital on investing in Canada.

The organizations include private investment firms such as Blackrock and some of the world's biggest sovereign wealth funds, including Singapore's GIC. Invitations were sent out this week, and none of the invited parties responded to CBC News before publication.

The summit is part of a broader effort to draw global investment back to Canada as the world grapples with deeper uncertainty and global volatility. Carney has been meeting with world leaders and private businesses during his trips abroad in an effort to attract more investment to Canada.

Part of the pitch is that, amid geopolitical turmoil, trade upheaval and conflict, Canada offers a reliable place to invest in ports, pipelines and infrastructure projects.

"Canada is in a really good place. Canada is cool again," said Michel Leduc, senior managing director and chief public affairs officer at the Canada Pension Plan Investment Board, which will host the meeting.

He said the summit will pitch "Canada, Inc." to investment firms looking for a safe, reliable place to grow in an increasingly unstable world.

"We want to showcase what Canada offers to the world of global investors," he told CBC News in an exclusive interview. "It's a little bit like a large public company holding their investor day."

Hopeful signs for foreign investment

The summit comes at a crucial time for this country.

For more than a decade, investment in Canada has lagged behind its peers. Canadian business investment was weak; some of Canada's biggest pension plans were spending more money outside the country; and large investors were putting more money abroad.

More recently, however, foreign investment in Canada has shown signs of picking up.

"Foreign direct investment in Canada reached the highest level since 2007, while Canada's outward investment flows cooled in 2025," wrote Maria Solovieva from TD Economics.

Part of the drop off in investment was, at least initially, due to the collapse in global oil prices in 2015. But critics say Liberal government policies at the time made the investment climate even worse by adding multiple layers of new regulation and uncertainty.

Carney has vowed to change that. He has promised to streamline the approvals process. He launched the Major Projects Office and designated a suite of plans as being in the national interest. They range from the Contrecoeur Container Terminal Project at the Port of Montreal to the McIlvenna Bay Foran Copper Mine Project in Saskatchewan.

Small window to attract new money

But business leaders in Canada say plans, memorandums of understanding and words alone are not enough.

Goldy Hyder, the CEO of the Business Council of Canada, said a summit like this is a good opportunity to promote Canada and help fund those kinds of projects.

He said the federal government has been saying many of the right things. But Canada needs to show investors that it is a country that can do and build big things — something he said it has repeatedly failed to do in the past.

Hyder said he hopes this time is different.

"If we don't get our resources out of the ground expeditiously in an investment-friendly regulatory climate, we are going to miss this window one more time, and I don't know how lucky of a country we think we are, but we don't have the nine lives of a cat," he said.

Leduc said he hopes the conference, tentatively titled the Canada Investment Summit, will establish long-term relationships with some of the biggest names in investing.

"It's a one- or two-day event, but it's obviously more than that. We hope that it's the start of something bigger, something exciting that will catalyze and create bigger opportunities going forward over many years," he said.

Not clear which projects will be pitched

Organizers did not want to get into which specific projects will be pitched and what, if any, projects are off limits.

"If you think of the big things we offer to the world — energy superpower, sovereign AI and data centres — we have one of the best financial sectors in the world," said Leduc.

While summit organizers have not said which projects will be pitched, business leaders and analysts broadly agree on the sectors where Canada is under pressure to attract capital most urgently.

The oil and gas industry has been calling for new investment in pipelines and LNG terminals. And despite a year's worth of talk, there's still no new proponent to build an oil pipeline to the West Coast.

New housing construction hit a new low last month in spite of the government's promises to build more.

And Ottawa has promised to spend more than $80 billion in the defence sector over the next five years.

Leduc said foreign investment firms have taken notice of Canada's plans. He believes the time is right for Canada to capitalize on that interest and draw in more investment from abroad.

The summit is set to be held in Toronto in mid-September. Invitations under Carney's name have been sent out. It's being co-hosted by the country's two biggest pension plans, CPPIB and PSP, in collaboration with Invest in Canada, an agency that promotes foreign direct investment in Canada.

But inviting participants to a meeting is a far cry from actually getting money invested in specific projects. As of publication, CBC News had not confirmed which, if any, of the invitees planned to attend.

Kathryn Mannie and David Baxter of the Canadian Press also report Carney announces new summit in Toronto aimed at driving $1 trillion in investment:

Prime Minister Mark Carney announced a new “Canada Investment Summit” that will invite investors, CEOs and business leaders to Toronto this fall.

The Prime Minister’s Office said in a media release the aim of the summit is to unleash $1 trillion in investment over the next five years to advance nation-building projects.

This comes after a globetrotting year for the prime minister, where he’s held several meetings with international investors and businesses in an effort to gin up interest in putting money into the Canadian economy.

Carney touted Canada’s strengths as an energy producer with a highly-educated workforce, saying Canada has what the world wants.

The goal of the summit is to grow businesses, unlock job opportunities and build a stronger economy, according to the release.

This comes after a decade of declining international investment in Canada.

A recent report from RBC says that last year was Canada’s first to attract more than $100 billion in foreign direct investment since 2015.

More than $1 trillion in foreign investment exited the Canadian economy between 2015 and 2024, what the report calls the “largest capital exodus in Canadian history.”

However, RBC projects Canada could attract upwards of $1.8 billion over the next decade if advancements are made in key industries. This includes building new pipelines and liquefied natural gas terminals, expanding nuclear, hydro and renewable power and growing as a critical mineral supplier.

The Canadian Federation of Independent Business issued a report this week pointing to a struggling small business sector in Canada. The CFIB says this is the sixth consecutive quarter they’ve tracked more small businesses closing than opening.

The Prime Minister’s Office says the summit will be hosted on Sept. 14 and 15 in partnership with the Canada Pension Plan Investment Board and the Public Sector Pension Investment Board.

The announcement comes as Canada faces ongoing economic disruptions due to the Iran war spiking gas prices and tariffs imposed by the U.S.

I would also recommend you read this RBC report, Capital Gains: How Canada can unlock the $1.8 trillion it needs for growth. Here are the key findings:

- Canada is back on the radar of global investors. Last year, foreign direct investment in Canada reached nearly $100 billion, the highest level since 2015.

- Global capital flows are shifting significantly. Geopolitical disruptions, most recently the conflict in Iran, are leading major investors and companies to rebalance their portfolios.

- A $1.8 trillion investment opportunity over the next 10 years could make Canada the G7’s growth leader. RBC Thought Leadership’s research and analysis indicates that there is an immense opportunity in six export-oriented, R&D-intensive, and strategically significant industries:

- Oil and Gas: $705 billion. New oil pipelines and LNG terminals could elevate Canada to energy superpower status, diversifying trade, providing energy security to allies, and fostering carbon capture and sequestration technologies.

- Oil and Gas: $705 billion. New oil pipelines and LNG terminals could elevate Canada to energy superpower status, diversifying trade, providing energy security to allies, and fostering carbon capture and sequestration technologies.

- Agriculture and Food Processing: $205 billion. Enhanced support for R&D could unleash a multi-decade, export-led growth cycle that strengthens domestic food sovereignty and enables food security to allied countries.

- Metals and Minerals: $200 billion. With NATO partners eyeing alternatives to a China-dominant critical mineral supply chain, Canada could hedge this concentration risk, power the West’s energy transition, and strengthen defence and advanced manufacturing supply chains.

- Defence: $19 billion. Canada plans to nearly triple defence spending to 5% of GDP by 2035, which could generate $100 billion for Canadian companies and transform Canada from a defence equipment importer into a contributor to allied military capabilities, particularly in emerging areas like Arctic surveillance and space-based defence systems.

- Space: $12 billion. Canada’s economic ambitions should extend out of this world. Investments in the space industry would advance the country’s excellence in satellite communications, space robotics, earth observation, and aerospace engineering, creating new opportunities in defence, high-tech and advanced manufacturing.

- Canada is emerging from an unprecedented capital recession. The renewed interest comes after a decade of weak business investment, stalling productivity, and stagnating living standards. Between 2015 and 2024, more than $1 trillion of investment exited Canada—the largest capital exodus in Canadian history. For every dollar of inward FDI, two dollars exited.

- To unlock investment, Canada needs a new capital formation framework. The non-financial corporate sector is sitting on more than $1 trillion in cash on its balance sheet. Its deployment could crowd in additional pools of capital: institutional, risk, foreign, and state capital. Our proposed capital formation framework includes four pillars, each targeting an incremental layer in the capital stack:

- A brownfield to greenfield asset recycling program

- Scale-enabling procurement

- Reforms to the corporate income tax and foreign investment regimes

- Leveraging of state capital

- Canada’s new playbook must include Indigenous economic partnership, which not only helps to secure project approvals, but can accelerate project timelines. Partnerships work best when they are embedded early and aligned with community needs.

Alright, it's Friday and I typically discuss markets today, but this is big news, and I promise to end off with some market comments at the end of my post.

So, big news, CPP Investments and PSP Investments will be hosting the first-ever Canada Investment Summit in mid-September.

Big investors will come, listen, but will they walk away convinced that Canada is a great place to invest in?

That, my dear readers, remains to be seen.

I'm not one to mince my words.

RBC Economics was polite to state, "Canada is emerging from an unprecedented capital recession."

Unprecedented is an understatement; it's been a disaster ever since Justin Trudeau's Liberals took power over a decade ago, slapped on a mountain of regulations, and killed all domestic resource projects.

Foreign investment plunged and there were zero resource projects under Trudeau's reign.

Now it's up to Mark Carney and his close-knit entourage of experts to clean up the mess they inherited, and while they're saying all the right things, so far, I haven't seen a lot of action.

The honeymoon is over. Words can only take you so far. Carney's Liberals need to deliver on new major projects. Period.

I personally want to see airports, ports, highways and other major infrastructure being privatized or risks being slashed to attract foreign and domestic investors.

We are at a point in Canada where if we do not do this, we are in deep, deep trouble (never mind what the IMF claims about our relatively strong fiscal position).

Buying off civil servants who want to retire early is easy. Attracting foreign capital is a lot harder.

If we don't fix the regulatory framework and entice foreign investors with great projects to invest in, they will not invest in our country.

It's that simple. And all the conferences in the world will not change this. Words and presentations alone will not change their propensity to invest in Canada.

Capiche? There is a ton of work to be done, and there are many hurdles to overcome before we attract one dime of foreign investment.

So, I welcome this conference, look forward to covering it, but colour me skeptical for now.At least Carney surrounded himself with competent people, which is more than I can say about Trudeau.

By the way, you can watch CPP Investments' Chief Public Affairs Officer, Michel Leduc, testify in front of the Standing Committee of Finance here.

Take the time to listen to Michel's comments and answers. He explains assets and liabilities of CPP, the role of CPP Investments to invest globally over the long run. He also discusses governance and what made the organization successful over time.

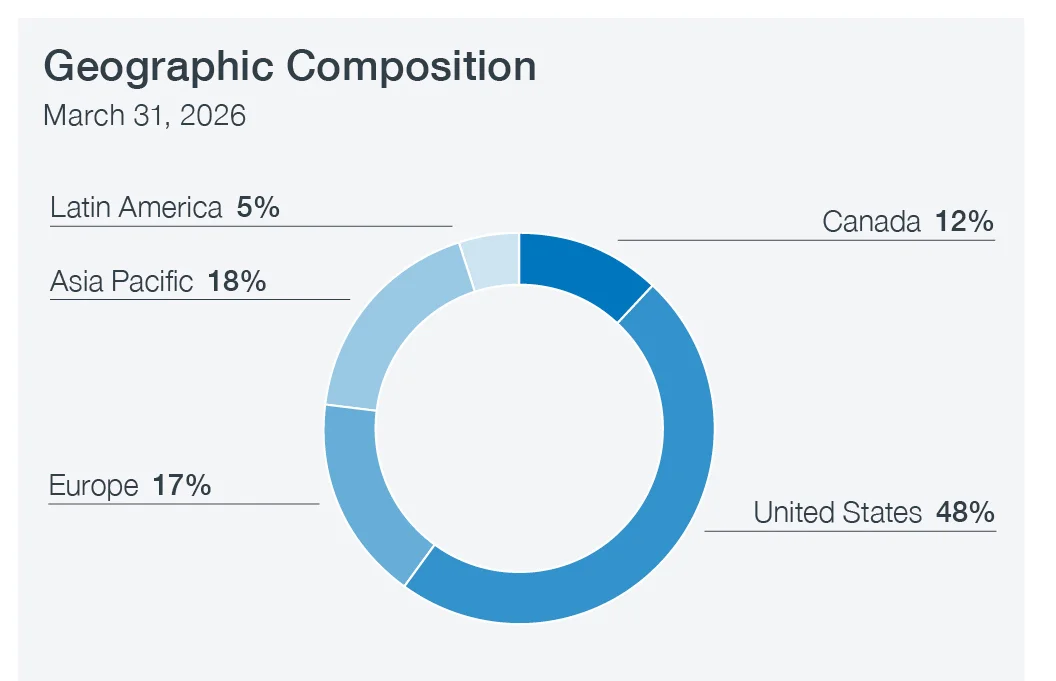

He also explains the concentration risk of Canada and why they need to invest globally but still invest significant amounts in Canada given their size.

Alright, take the time to watch it here (you can change from French to English on the bottom left corner, just click on the language and choose the one you want).

Let me quickly shift my focus to markets.

Here is the major story today: oil drops, stocks soar to wrap up a wild week.

The S&P 500 notched its first close above 7,100, and the Nasdaq posted longest win streak since 1992.

Everything except energy stocks was on fire today after Iran declared the Strait of Hormuz “completely open” on the heels of a ceasefire announcement between Israel and Lebanon.

But late Friday, there remains considerable confusion as a video shows ships turning away from the Strait of Hormuz as confusion persists over whether sea lane is really open.

We shall see where this goes next week but many investors are exasperated with the yo-yo market.

⚠️THIS IS ABSOLUTELY INSANE:

— Global Markets Investor (@GlobalMktObserv) April 17, 2026

The Nasdaq 100 index has gone from oversold to OVERBOUGHT levels in just 2 weeks, measured by the Relative Strength Index (RSI).

This comes as the Nasdaq 100 has recorded 12 consecutive green sessions, the longest streak in 13 YEARS.

This is the… pic.twitter.com/Lg71Nftboz

The S&P 500's recovery rally is now the fastest since 1982. pic.twitter.com/nGitzH0IUa

— Hedgeye (@Hedgeye) April 17, 2026

Clearly, algos are running this market, jumping on everything Trump says or posts on his social media platform.

Alright, let me wrap it up quickly with the top-performing US large-cap stocks this week (full list here):

I wouldn't chase any of them here but definitely keep an eye on them.

Next week, we get big tech earnings reports. It will be interesting to see the reaction following earnings.

Below, Investment Committee debate how to position your portfolio after Iran's Foreign Minister declared the Strait of Hormuz will remain open during the ceasefire.

Also, Morgan Stanley's Katerina Simonetti joins 'Fast Money' to talk the state of the market, hurdles for the rally, and what she is looking at for both the near and long-term.

Third, Bob McNally, president and founder of Rapidan Energy Group, said that despite oil market optimism, he believes the Strait of Hormuz will close once again unless the US and Iran make major progress on a deal over the weekend. McNally said that his estimate is that it will take at least 3 to 4 months for the oil market and supply traffic to revert back to pre-war levels once there is a deal and that there are some oil fields that may be permanently closed.

Fourth, Natasha Hall, associate fellow at Chatham House, said that despite positive reaction to the announcements from the US and Iran, the ceasefire is very fragile and there are many complex details still to be worked out. Hall said that there are potential 'spoilers' that could emerge in negotiations as Iran considers nuclear restrictions and its newfound economic power via the Strait of Hormuz.

Lastly, Jim Bianco discusses the persistence of a "permanent risk premium" in financial markets, driven by geopolitical tensions between the US and Iran, even if a temporary ceasefire holds with Lisa Abramowicz and Annmarie Hordern.

“Deliberate

credit selection, as opposed to broad market exposure, is where

long-term value is created within private credit. You don’t just go out

and buy a slice of the market—if you do that, you face very tight credit

spreads and poor credit selection. Since the portfolio’s inception in

2018, our focus has been on the quality of the portfolio, across

geographies, structures, and market cycles, a discipline that positions

us well in this market and is reflected in the returns we deliver for

our clients.”

“Deliberate

credit selection, as opposed to broad market exposure, is where

long-term value is created within private credit. You don’t just go out

and buy a slice of the market—if you do that, you face very tight credit

spreads and poor credit selection. Since the portfolio’s inception in

2018, our focus has been on the quality of the portfolio, across

geographies, structures, and market cycles, a discipline that positions

us well in this market and is reflected in the returns we deliver for

our clients.”  “I’m

cautiously optimistic, moving towards more optimistic on private equity

as deal activity slowly recovers. BCI has had a great ten-year

run—returns around 16.1%. The platform is well positioned for the market

opportunity going forward.”

“I’m

cautiously optimistic, moving towards more optimistic on private equity

as deal activity slowly recovers. BCI has had a great ten-year

run—returns around 16.1%. The platform is well positioned for the market

opportunity going forward.”  ”BCI

Infrastructure & Renewable Resources has navigated through a number

of bumps in the road—the global financial crisis, euro crisis, COVID,

post-COVID inflation. Part of the reason is the highly diversified

portfolio across many sectors and countries. When you look at the

portfolio level, it’s very resilient.”

”BCI

Infrastructure & Renewable Resources has navigated through a number

of bumps in the road—the global financial crisis, euro crisis, COVID,

post-COVID inflation. Part of the reason is the highly diversified

portfolio across many sectors and countries. When you look at the

portfolio level, it’s very resilient.”